Borrowing costs, the dollar, major stock markets and Bitcoin all rose this morning as markets absorbed the victory for Donald Trump in the US presidential election.

The yield on American government bonds, a key benchmark for the global financial system, rose by about a fifth of a percentage point to almost 4.5% for 10-year borrowing. The dollar rose by 1%-2% against key currencies such as the yen and euro while stock markets in Japan and Australia gained as weaker currencies help exporting nations. Stock markets in China and Hong Kong fell, however, as investors reacted to the likelihood of significant tariffs on their exports to America.

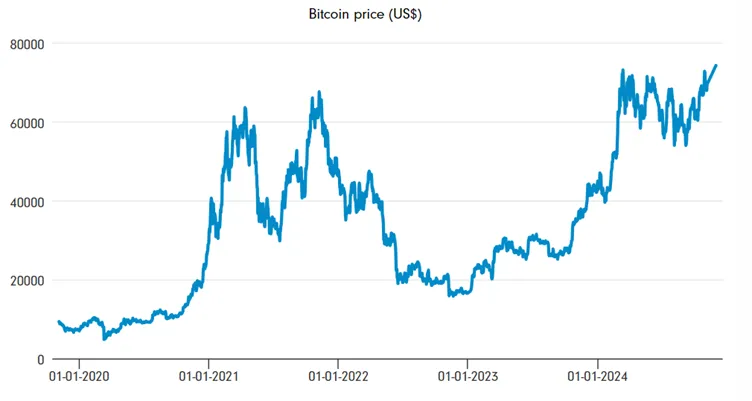

The price of gold retreated by about 0.8% but Bitcoin reached US$75,000 for the first time thanks to Mr Trump’s endorsement of the cryptocurrency.

Bitcoin price (US$)

Source: Investing.com, 6 November 2024, bitcoin price in $USD

Past performance is not a reliable indicator of future returns

Oil prices fell as the market reacted to the election of a president who has promised to ‘drill baby drill’ in an attempt to lower fuel costs for American consumers and perhaps erode the power of rival producers such as Russia and Iran.

Although Mr Trump is now certain to re-enter the White House we still don’t know whether his party has won the House of Representatives, the lower house of the American Congress. While Mr Trump has gained control of the upper house, the Senate, a president who wins both houses is hugely more powerful – he does not have to seek compromise with the opposing party in Congress to put his policy programme into practice. It is possible that a ‘clean sweep’ for the Republicans of the presidency, the Senate and the House of Representatives could propel ‘Trump trade’ winners such as the dollar higher still.

What is the ‘Trump trade’?

The Republican candidate has promised to ‘end inflation’, cut taxes and interest rates, reduce immigration and impose tariffs on imported goods such as Chinese electric cars. But markets see these goals as incompatible and instead are betting on higher inflation and higher interest rates.

And while Mr Trump has promised to cut what he calls wasteful state spending, perhaps by appointing his key ally Elon Musk, the boss of Tesla, to his government, some economists fear that his populist instincts are more likely to see America’s already huge budget deficit grow still further. Such a development is also seen as inflationary by economists because it amounts to the government pumping money into the economy.

They say that tax cuts will boost consumer spending, which will put upward pressure on prices as more money chases the goods and services available, while cutting immigration or even deporting illegal immigrants will cut the supply of labour and push wages higher. Tariffs on imported goods also increase prices for consumers. Although increased oil supply would work in the other direction, it will take time for new oil wells to start producing.

Fears of a rise in inflation lead to expectations of higher interest rates to counter it. This explains the rise in the yield on American government bonds and will focus investors’ attention on the interest rate decision of the Federal Reserve, America’s central bank, tomorrow.

How different stock market sectors are likely to react to Donald Trump’s victory

In pre-market trading in America, shares in Tesla, Elon Musk’s electric car maker, soared by as much as 14%, which would add about US$113bn to its valuation. Not only is Mr Musk a close ally of Mr Trump but the latter has made tariffs on foreign products such as Chinese electric cars a centrepiece of his campaign for re-election. Mr Musk also supports the Republican candidate’s plans for deregulation, which could help innovative companies such as Tesla and SpaceX, his space exploration business.

Prospects for the other ‘Magnificent 7’ stocks are less clear-cut, although high-growth companies tend to suffer from rising interest rates for technical reasons: rising rates cause investors to ‘discount’ the value of their future earnings more severely.

American oil stocks rose in pre-market trading despite the fall in crude oil; shares in Exxon, the biggest US oil company, gained about 2.8% and others followed suit. This may be because investors expect an easier regulatory ride from the new administration. Larger volumes from US oil production may also offset lower prices. In Britain, Shell trod water while BP gained about 1.3% in morning trading.

Clean energy looks likely to be punished by the new President Trump and stocks in the sector have taken a battering. Vestas Wind Systems, the Danish wind turbine maker, lost about 8.5% and rival firm Nordex of Germany fell by 6.3%.

What about the longer-term impact on stock markets?

The evidence suggests that the choice of president has little influence on Wall Street. ‘The big conclusion for me is that, over the long term, who is sitting in the White House doesn't matter for the economy,’ Rosanna Burcheri, portfolio manager at Fidelity said. However, Mr Trump does regard the stock market under his tenure as an indicator of his success as president.

A strong dollar and high American interest rates can, however, have significant effects on overseas stock markets. The FTSE 100 tends to rise as sterling falls but emerging markets are even more exposed: they may have borrowed in dollars, which makes depreciation of their own currencies painful, and their borrowing costs are often linked directly or indirectly to American interest rates. The combined effect can be extremely damaging to emerging economies. Investors may want to take a longer view before they react to today’s momentous political events, however.

Historically, financial markets have largely been unbothered by presidential elections. Naveen Malwal of Strategic Advisers, who manages money for many of Fidelity Investments’ clients in the US, said: ‘It can be tempting to attribute market volatility to politics, but while political headlines may at times cause short-term ripples in the market, long-term, for stocks, bonds, and other investments, returns seem to be driven much more by the fundamentals of the underlying asset classes.’