One of the first things fixed income investors must do is determine the risk profile of a bond. In this article, we look specifically at corporate bonds and their two main risk classifications: investment grade and high yield.

Not all bonds are the same

It is widely accepted that bonds classified as investment grade tend to be less risky than those designated as high yield and usually deliver a lower return. High yield bonds typically offer higher returns, but with more risk, because the issuers are considered to have a greater chance of default. As a result, these companies pay higher coupons to reflect the additional uncertainty associated with their debt. For example, bonds issued by a relatively young technology firm or an ambitious property developer would likely be classified as high yield.

Different types of bonds are likely to appeal to different people. Someone in their 20s, who has a long investment time horizon to recoup any capital losses, might include high yield issues in their diversified portfolio. Conversely, investment grade bonds – like government bonds – may find favour with an older investor, who is nearing retirement and looking to preserve capital.

The classification of bonds

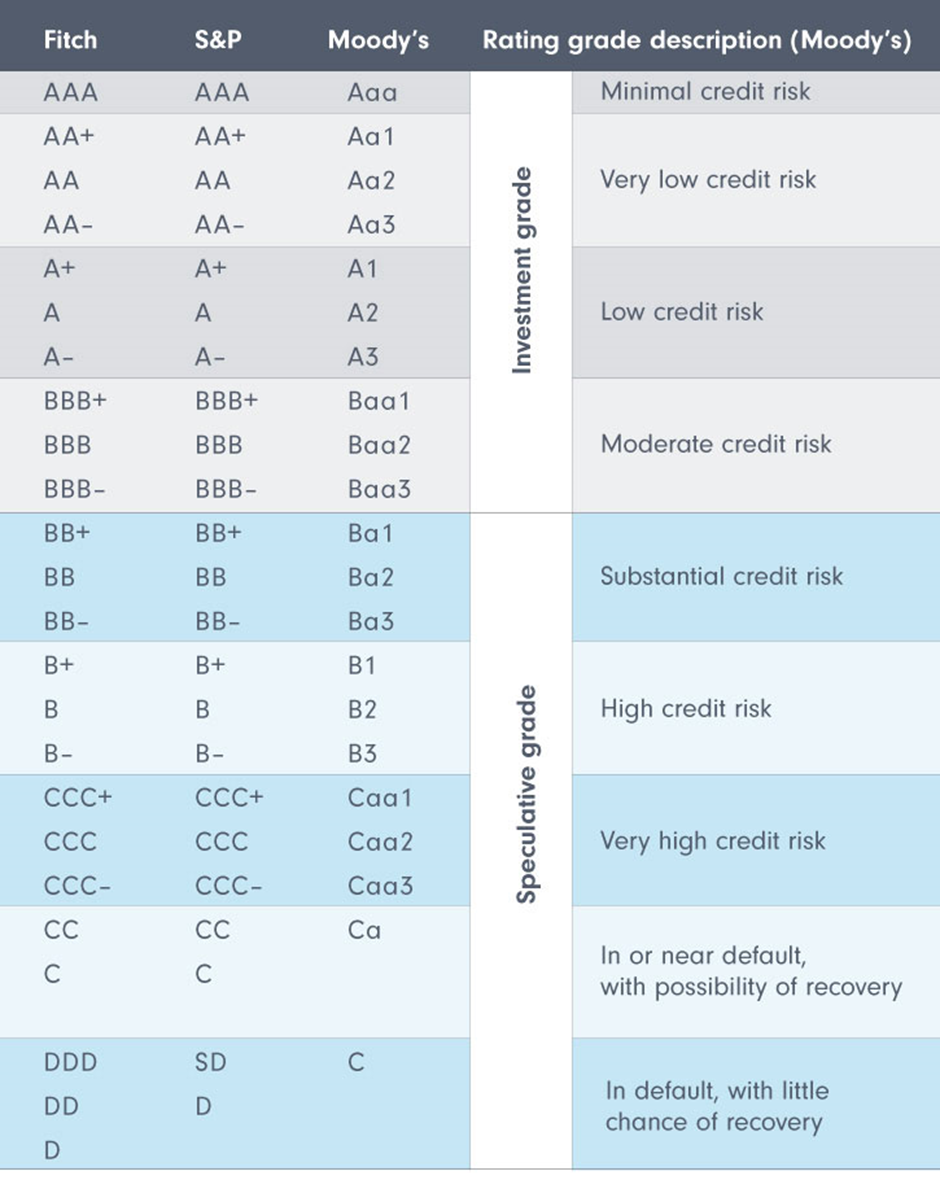

The good news for investors is that it is relatively straightforward to generally assess the risk profile of a bond, with much of the detailed research carried out by external credit rating agencies. The three most significant firms in the market are Standard & Poor’s (S&P), Moody’s and Fitch, who screen the bond universe to decide which are investment grade or high yield instruments.

If we take S&P’s classification system as an example, it assigns different credit ratings, based on how much risk is attached to the repayment of capital. These comprise one to three letters such as ‘AAA’, ’BB’ or ‘C’ (with ‘+’ or ‘–’ signs providing further differentiation).

There is a dividing line: bonds with good credit ratings of at least ’BBB –’ are classed as investment grade bonds, while those below ‘BBB–’ are treated as high yield bonds (also known as speculative or junk bonds).

Moody’s rating scale is slightly different from but broadly similar to that of Fitch and S&P.

As an aside, government bonds are classified in much the same way. Therefore, the US’s debt might be ranked investment grade with Venezuela’s deemed high yield.

Bonds’ credit ratings may also be upgraded or downgraded over time. Therefore, investment grade bonds could become high yield bonds – the so called ‘fallen angels’.

How does the economy impact different bonds?

Investment grade bonds are usually favoured when economic conditions are deteriorating. However, under buoyant conditions, demand for high yield bonds increases. Amid stronger global growth, higher yielding bonds have generally outperformed lower yielding ones.

Interest rates and their effect on a bond’s rating

Duration, which is often measured in years, is calculated by time weighting the bond investor’s expected income (or coupon) and maturity (or principal) payments. Bonds with higher durations are more sensitive to actual, or expected, changes in interest rates than bonds with lower durations.

Investment grade bonds usually have higher durations, because proportionately more of their total income stream is received via the repayment of principal at maturity. The most attractive investment grade bonds are similar to high quality government bonds (which also tend to have above average durations).

With high yield bonds, proportionately more of the payments are received by way of coupons, and their maturities are typically shorter. Therefore, when interest rates rise or are expected to, they tend to be less affected than investment grade bonds. However, when interest rates fall or are expected to, the prices of high yield bonds are likely to rise by less than prices of investment grade bonds.