- Private equity is still the largest raising asset class, and given how quiet the IPO (initial public offering) markets have been we believe mid-market provides the best risk-return options

- Infrastructure is likely to provide more opportunities as growth in digital infrastructure and renewable energy assets is supported by the supply-demand imbalance across both sectors

- Senior direct lending continues to offer interesting options for exposure to secured private loans, with interest rates expected to stay at relatively raised levels for longer

- Real Estate: European office space is on the verge of its recovery and with prices currently low has potential for strong returns over the next two to three years

Private assets are on the cusp of a new cycle and we expect the first half of 2025 to offer up attractive prices for what promises to be a strong vintage of investments.

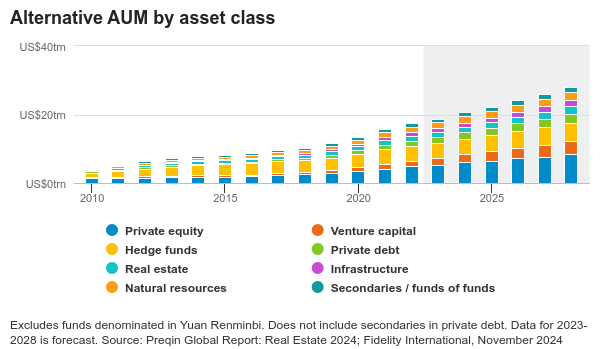

It will be a cycle where private markets come into their own. The asset class has conclusively left its niche reputation behind, with extraordinary growth globally over the last five years. The range and sophistication on offer to investors – no matter what their strategic priorities – are reaching a new level of maturity.

As in the public markets, investors can build their private portfolio based on their own risk-return profile. Growth-oriented investors can opt for high allocation to private equity funds - whether buyout, growth, or even venture strategies - while an income-focused investor will tend to add private credit or core infrastructure exposure that will provide a steady return of distributions. A diversified private assets portfolio can combine all asset classes.

A turnaround story

We anticipate that 2025 will be a good year for private equity. After years in which buyout activity has been stymied by global volatility, the pent-up demand for new deals and the strong financing bid are all likely to contribute to a higher level of deal-making. We’re already seeing this in the US, and we expect to see it in more heavily-regulated Europe too, even though it tends to be more defensive, particularly across software, technology, and services sectors.

Any uptick in new private equity-backed buyouts will of course also improve the prospects for direct lending funds that finance and sponsor these Merger & Acquisition (M&A) deals, and for the buyout funds that already make up the majority of the private equity market.

Direct lending has enjoyed plenty of attention in recent years thanks to high interest rates. Although that backdrop is likely to shift in 2025, all of the European and US general partners (GPs) we’re speaking to report their direct lending funds are still growing. Returns are fading from the 10-11 per cent that was offered a year ago when liquidity was more stretched, but direct lending GPs returns are holding at around 7-9 per cent - clearly still very compelling.

Given the diversification now offered in the private credit universe there is certainly a strong case for its inclusion in a portfolio. Some 96 per cent of European companies with revenues over US$100 million remain unlisted1, while globally the median age of a company at IPO has shifted from four years in 1999 to 12 years in 20202.

For those investors looking for further ways to diversify, the increasing maturity of the secondaries market may be interesting in 2025. Once a speciality product used only by distressed sellers, secondaries has now become a huge market that offers access to holdings of previous vintages.

GP-led transactions have become more common here - now making up around half of the market globally - and are likely to continue in 2025 across private equity, credit, infrastructure, and real estate, as managers roll their holdings into different vehicles to release any available financing.

Strong and steady

Elsewhere, if an investor is looking for more stability in a portfolio, infrastructure and real estate offer long-term investments with attractive entry prices available in the first half of 2025.

The two big drivers of the infrastructure market at the moment are digital assets and the energy transition. The increase of data consumption will be further enhanced by artificial intelligence (AI) and by growing renewable energy demand, while the evolution of AI also means more data centres (and so more infrastructure opportunities) and further investment in private equity-backed software firms.

There are questions about how the energy transition program will develop in the US under the new administration, but given that some of the biggest planned projects are in red states, we do not expect these to be cancelled altogether. Europe still has a much stronger focus on the transition, whereas midstream and traditional energy continues to play more of a role in the US market.

The turnaround in private assets in 2025 is likely to be most noticeable in European real estate. We believe now is a wise time to get into the market given there are low prices and plenty of assets available. The growing importance of logistics has been well documented, and rightly so: the widescale adoption of online shopping, accelerated by lockdowns, and the nearshoring of supply chains will boost demand for warehouses across the year.

But we have particularly strong conviction in the prospects for the offices sector, especially in the brown-to-green strategy of renovating buildings to become more carbon-neutral, and in particular for those portfolios that do not already hold office assets.

Although both the US and European markets are dislocated going into the new year, the level of oversupply in US offices has been far higher, and the market there for this subsector looks less attractive than Europe. But we do also expect to see more demand for residential assets across both Europe and the US due to structural undersupply.

Read more articles from our 2025 Outlook