Companies are entering a new phase in their approach to environmental, social, and governance (ESG) issues, responses to Fidelity’s 2024 Analyst Survey show.

“I think investors and lenders have been very lenient to date, understanding that establishing an ESG framework, setting up a committee, confirming goals and so on were the first steps, and that being ‘early adopters’ was seen as a positive,” says Liz Brockway, a private credit analyst who covers the European chemicals sector. “Now the focus is moving to execution and delivery of these goals and promises.”

From 2024, large companies in the European Union will need to track how their activities affect the environment and society in order to comply with the Corporate Sustainability Reporting Directive, and then start reporting this information annually in 2025. Meanwhile, global reporting standards developed by the International Sustainability Standards Board come into effect this year. Companies also face reporting requirements devised by the Task Force on Climate-related Financial Disclosures.

“Five years ago, the oil and gas industry was quite dismissive in its approach to ESG, but companies have really changed their view.”

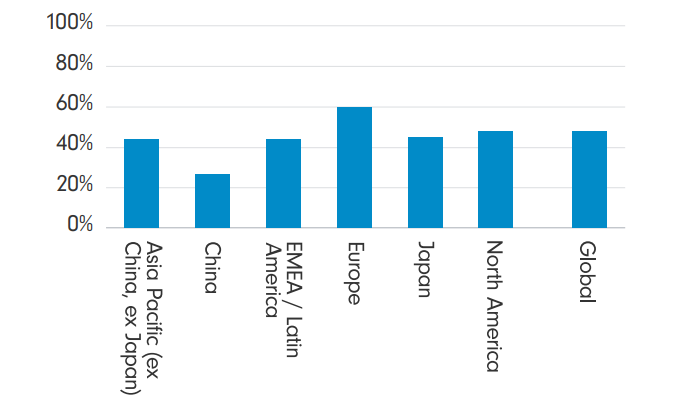

Many businesses still have a lot of work to do. Across all regions, analysts say that only about half of their companies are ready to meet their sustainability reporting requirements. This rises to around 60 per cent for analysts covering European firms, leaving many unprepared even in the most prepared region of the world.

Firms falling short on future reporting requirements

Chart shows responses to the questions: 'Starting in 2024, large companies around the world will have to fulfil new corporate sustainability reporting requirements (e.g. CSRD, ISSB, TCFD). What percentage of your companies would you estimate are ready to meet their respective reporting requirements?'

There is a risk that all these new rules are seen as moving the goalposts. Compliance will place a burden on companies. But there are advantages to developing a set of rules and reporting standards that will help prioritise companies’ actions, a sentiment our analysts often encounter as part of their company engagements.

Currently, “investors have different ESG agendas and companies don’t know which ESG areas to spend more time and money on,” explains European retail analyst Serhat Birbilen. “It is hard for companies to focus on so many different ESG issues and they seem to be struggling in allocating the resources to the causes that generate the highest return for the environment and society.”

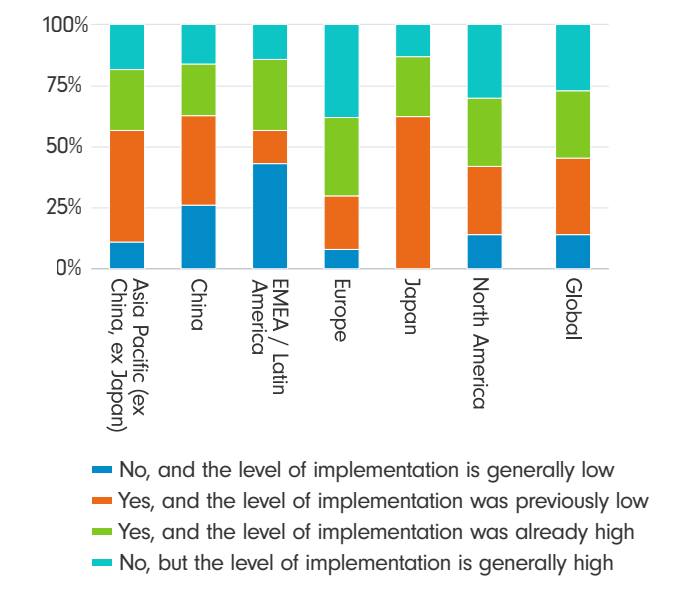

Growing implementation

Despite these challenges, companies continue to make headway. Nearly a third of analysts say ESG implementation at their companies has improved from levels that were previously low. A further 28 per cent report improvement from already high levels, while 27 per cent say that ESG implementation was already high leaving little room for discernible improvement in 2024.

ESG implementation continues to improve

Chart shows responses to the question: 'Have you seen a growing emphasis among your companies to implement ESG policies in the last year?'

Specific examples analysts cite include L’Oréal shifting away from its reliance on petrochemicals, with a target to ensure that 95 per cent of the chemicals used in its products come from plant-based ingredients (it is currently at around two thirds).

Elsewhere, Alexander Laing, a utilities analyst, notes: “Vestas has recently developed the first technology to break apart epoxy bonding resin for its wind turbine blades which means that these can be recycled for the first time. This has been a major issue for end-of-life in this industry until this point.”

Changes in the energy sector

One of the biggest environmental challenges is also arguably the highest profile: reducing the emissions of the energy sector. Here too we see some evidence of progress, despite the often-depressing headlines.

“Five years ago, the oil and gas industry was quite dismissive in its approach to ESG, but companies have really changed their view,” says Thomas Goldthorpe, an equity analyst covering energy in North America. “They’re being proactive – proving willing to invest, willing to cut emissions, and willing to be a stakeholder at the table. They’re serious about reducing their scope 1 and 2 emissions.”

But while the industry may now be improving the efficiency of its exploration, production, and refining processes to reduce its scope 1 and 2 profile, that still leaves scope 3 emissions to be dealt with; those produced by the use of fossil fuels in society. These emissions are easily the most significant, and tackling them is not about dealing with the energy firms themselves but rather about focusing on where demand is coming from, ensuring that industry and society is decarbonising to reduce their reliance on energy produced by fossil fuels.

There still needs to be much more progress in substituting fossil duels for alternatives and Fidelity will continue to work with companies that are end-users (particularly those in hard-to-abate sectors such as heavy industry and transportation) to improve the efficiency of their processes.

Progress for firms in the energy industry itself remains a challenge. Last year, some high-profile companies rowed back on their commitments to tackle the intensity of their emissions or to increase their capex spend on sustainable processes. But there are some glimmers of hope that the looming energy transition is still driving some behaviour in this sector.

“It’s no coincidence that ExxonMobil recently announced larger targets for its own clean energy capex,” says Paul Gooden, another equity analyst covering North American energy firms. “For a Western oil major to say that around 25 per cent of its capex will be spent on low emissions projects by 2027 is remarkable. Around half of this will be spent on reducing the company’s own emissions and half on reducing third party emissions via biofuels, carbon capture and storage (CCS), and from hydrogen projects.”

As part of this effort, ExxonMobil recently completed the takeover of Denbury, which owns and operates the biggest network of CO2 pipes in the US, increasing Exxon’s CCS capabilities.

CCS appears to be a natural way for oil and gas firms to play a role in the energy transition - and not just because it provides a green argument for their continued operation.

“Being a utility is not what big oil does,” says fixed income energy analyst Randy Cutler. “Big oil understands geology and that’s what CCS is.”

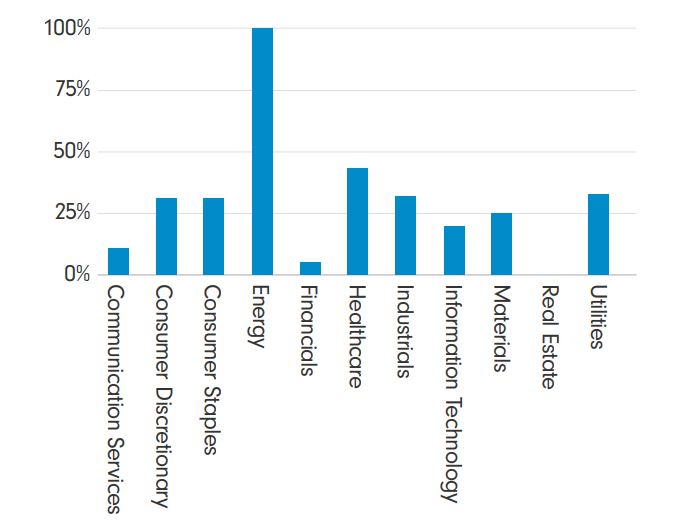

The Denbury deal was only part of a wave of M&A in the sector that looks set to continue. Every one of our energy analysts expects major strategic M&A in their sector this year.

Energy industry readies for strategic M&A

Chart shows responses to the question: 'Where you are seeing M&A, what type is it? (Please select all that apply).'

To be clear, analysts do not believe that the main driver for this wave of M&A is sustainability, but rather valuations. Bigger companies on higher multiples are well placed to snap up cheaper rivals, looking to boost cashflow without adding to overall supply (which could push down energy prices).

But the energy transition is also on everyone’s mind. For large players it puts a question mark over big projects, which incur tens of billions of dollars in capex upfront, take several years to start generating cash, and then pay back over several decades. And for smaller companies, it’s one more incentive to listen to suitors while their chequebooks are open.

“If you’re a small company, what are the odds of surviving an energy transition?” asks Cutler. “It’s better to sell now.”

Companies staying the course

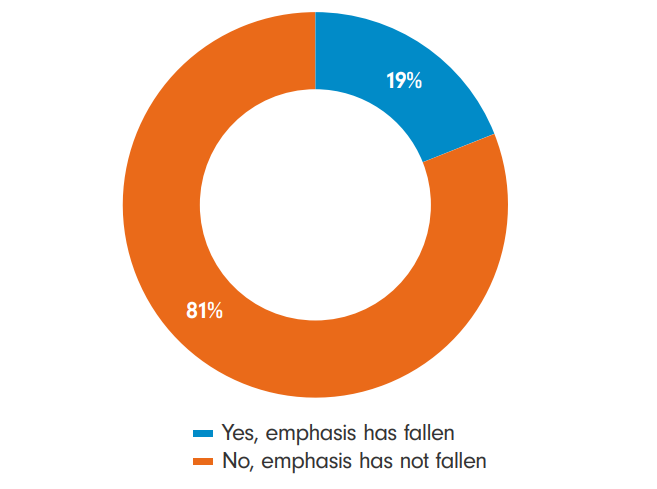

Perhaps the most compelling ESG finding in this year’s survey is also the simplest. We asked analysts if the emphasis on sustainability among their companies has fallen in the last 12 months. Some analysts do say they have seen signs of ESG fatigue, while others suggest economic and geopolitical headwinds are drawing focus elsewhere.

Nonetheless, four out of five analysts say that no, the emphasis has not fallen among the companies they cover.

A firm focus: companies continue emphasis on ESG

Chart shows responses to the question: 'Has the emphasis on ESG among your companies fallen over the last 12 months?"

That’s good news. Because it’s not just reporting requirements that are likely to become more challenging in coming years. ESG is a key aspect of a company’s societal license to operate and its ability to create long term value for stakeholders. Businesses must be prepared to continue to tackle this increasingly demanding environment.