War, inflation, impending recession - 2022 was a test of companies’ commitment to sustainability while fighting other fires.

Encouragingly, the vast majority (90 per cent) of Fidelity analysts report their companies are placing the same or greater emphasis on environmental, social, and governance issues (ESG) as they were a year ago. But elsewhere in the survey we find that on urgent issues, like protecting oceans and ending deforestation. companies have a lot of room to improve. And without action we may lose the battle against climate change.

ESG still on the radar

“Russia-Ukraine might have changed the conversation a bit,” says one Europe-focussed materials sector analyst, “but it has probably just slowed [progress on ESG] down as opposed to reversing them.”

“Pretty much every company now has ESG on their radar and is setting it as a priority,” confirms an analyst who covers Asia Pacific energy companies, a sector that has traditionally lagged in this area.

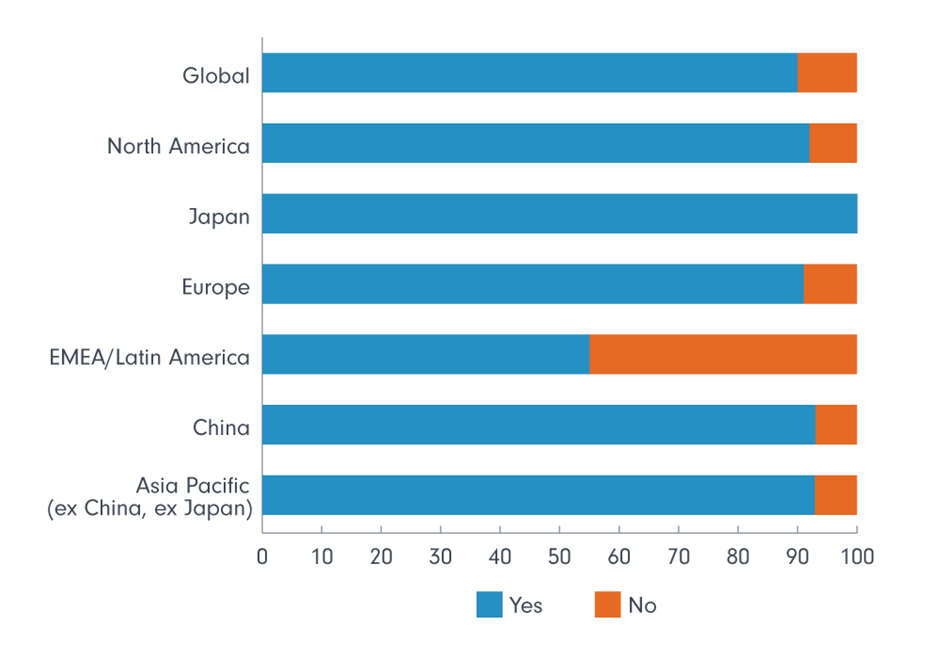

Chart 1: Companies have maintained their ESG focus

Question: “Has the emphasis on ESG among your companies fallen over the last 12 months?”

There are a few exceptions. Nearly half of EMEA/Latam analysts report a reduced emphasis on ESG among their companies compared with a year ago. One industrials analyst explains that the companies she covers “are just trying to stay afloat” and therefore “ESG has taken a back seat”.

“There are more pressing issues to talk about,” adds another EMEA/Latam analyst, referring to conversations with the financial firms he speaks to in the region.

This sentiment is repeated sporadically even in regions where ESG is more established. One analyst who covers European industrials says: “Companies are more focused on supply chains, inflation and other matters.”

Overall, though, to quote one information technology (IT) analyst: “Companies are clearly improving their ESG communication, probably in response to increased investor attention.”

Carbon neutrality still a distant goal for most, but companies are acting

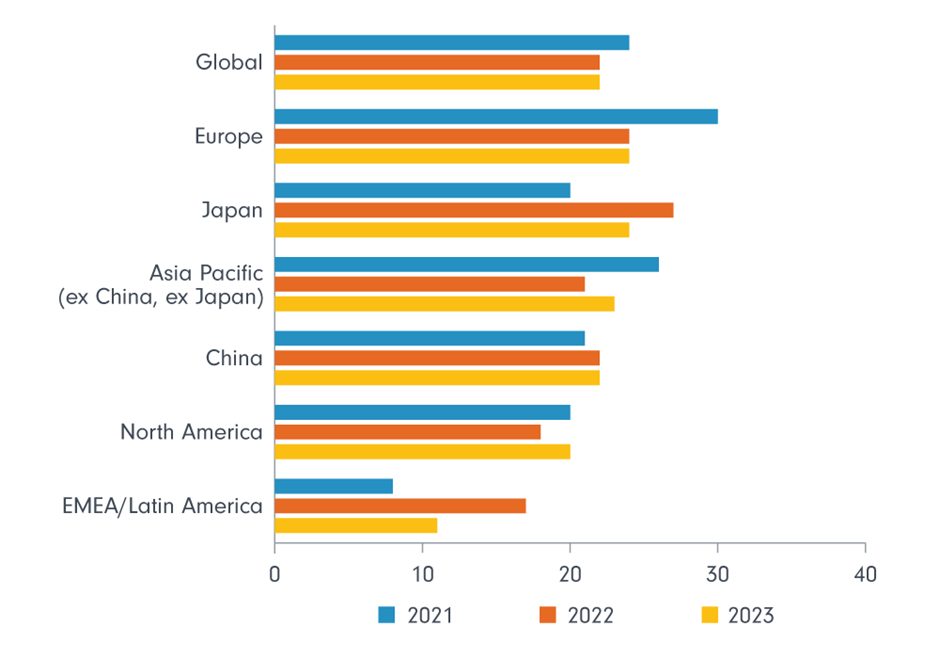

Talking about ESG is one thing. Translating it into real-world progress is another. As Chart 2 shows, at a global level, our analysts expect only 22 per cent of the companies they cover will be carbon neutral by 2030 - a percentage that hasn’t moved from last year.

Chart 2: Less than a quarter of companies expected to be carbon neutral by 2030

Question: “What percentage of your companies do you estimate will be carbon neutral (scope 1, 2 and 3 emissions1) by 2030?”

As we noted in last year’s survey, companies are getting better at assessing what is required to reach net zero, and the lack of movement in this headline number masks a lot of progress below the surface.

Responding to the 2023 survey, one analyst covering North America’s consumer discretionary sector tells us: “Each year companies are gradually learning more and communicating more about ESG. While this is still not a core focus for most companies in my coverage, it is something they've gotten better at thinking about and talking about.”

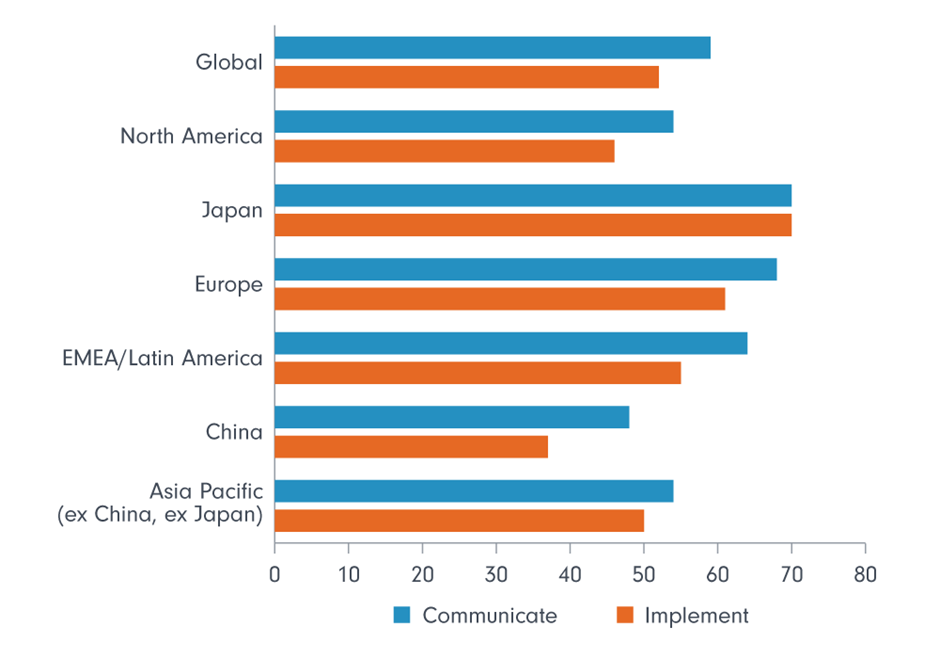

Companies are also taking active steps to improve their ESG credentials. As Chart 3 shows, more than half our analysts say the majority of their companies are better at both communicating and implementing ESG policies than they were a year ago, and most of the rest detect improvement in at least some of their coverage. Interestingly, our survey also finds a strong overlap between companies that communicate their ESG policies and those that follow through and implement them.

Chart 3: More companies are both saying they’ll do more and following up with action

Questions: “Have you seen a growing emphasis among your companies to communicate ESG policies in the last year?” and “Have you seen a growing emphasis among your companies to implement ESG policies in the last year?”. Chart shows the percentage of analysts who report a growing emphasis at a majority of their companies in the last year.

Commenting on the improvements he’s seen, one North American consumer staples analyst says: “Many companies have made new commitments, including net zero targets, and a few have added ESG metrics to executive compensation.”

One financial sector analyst meanwhile notes that “more banks are issuing Task Force on Climate-related Financial Disclosures (TCFD) reports”, which help investors and others better see how a company is exposed to climate risks and opportunities.

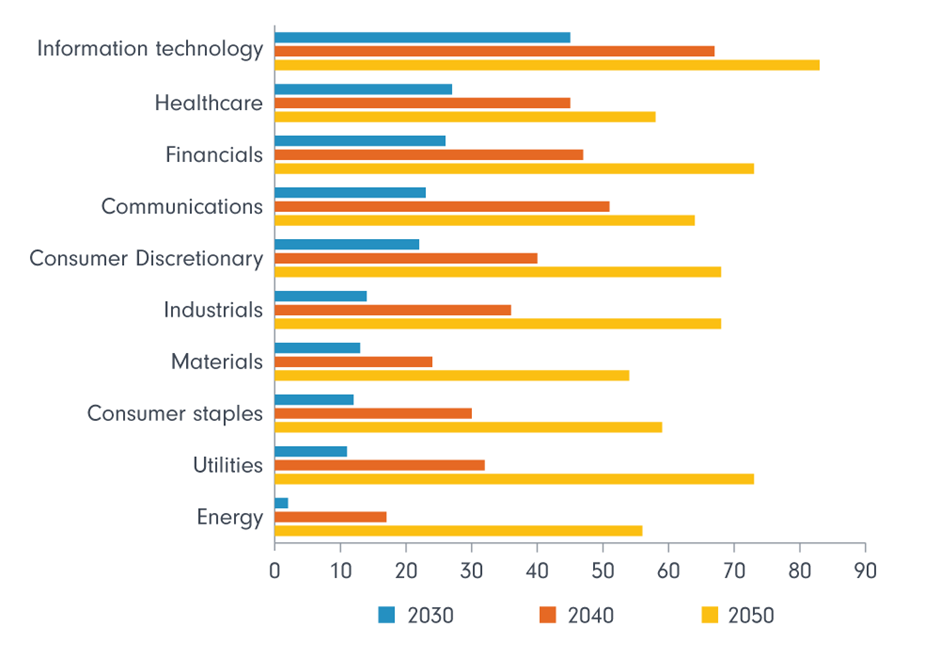

Over time, a lot more companies are expected to move towards net zero, even if most will take until beyond 2030 to get there. Our analysts expect 42 per cent of companies globally will be carbon neutral by 2040 and 68 per cent by 2050. This is taking into account all emissions associated with a company’s activities, not just those the company creates directly but those up and down its value chain too. Consider, too, that some of those not expected to be carbon neutral in 17 or 27 years’ time may no longer exist and we may be looking at a profound shift.

Perhaps not surprisingly, it is in sectors with harder-to-abate emissions, such as materials and energy, where analysts expect more muted progress.

Chart 4: Hares and tortoises in the race to net zero

Question: “What percentage of your companies do you estimate will be carbon neutral (scope 1, 2 and 3 emissions1) by: 2030, 2040 and 2050?”

Despite the challenges (or indeed because of them) our analysts are engaging fruitfully with company managers.

“Oil and gas companies understand that ESG is a requirement for listed fossil fuel companies and almost all have plans for net zero scope 1 and 2 emissions by 2050,” says an Asia Pacific energy analyst, referring to companies’ direct emissions (scope 1) and the indirect emissions from purchased electricity used by companies in their operations (scope 2).

However, “treatment of scope 3 emissions differs a lot”, the same analyst observes. In other words, some companies are doing a better job than others of working to address the emissions caused by those using their product, which in the case of fossil fuels is where most emissions happen.

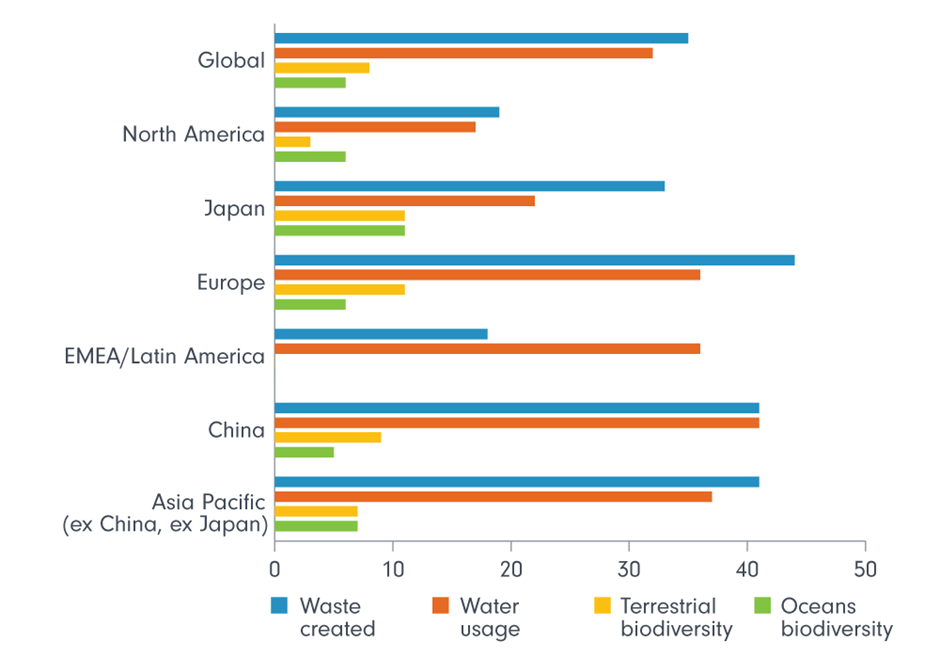

Nature calls

Despite ongoing progress towards net zero, there is one area that appears to have had too little attention. Reducing emissions is just one side of the climate change equation. On the other is the urgency of reversing nature loss and protecting forests and other carbon sinks. Only 8 per cent of analysts expect companies to reduce their negative impact on terrestrial biodiversity within the next 12 months. For oceanic biodiversity the figure is 6 per cent.

Chart 5: Biodiversity has been on the back burner up to now*

*X-axis = Proportion of analysts expecting companies to reduce impact on the listed areas

Question: “To what extent do you expect your companies to reduce their negative impact on the following areas over the next 12 months?” Chart shows proportion answering 5-7 where 1 means will not reduce their impact and 7 means will significantly reduce their impact.

“Initiatives related to biodiversity are still in early stages for most companies”, says one analyst. “Water and waste management has more direct benefit to the business from a cost savings perspective and companies tend to be more motivated to address those areas.”

We are encouraging managers we meet with to recognise the incentives to their business of addressing nature-related risks as well, be they physical risks to which their supply chains are exposed, or legal and reputational risks arising from new regulations and the changing expectations of customers, investors, and the wider community.

Moreover, preserving and restoring natural capital is seen as a necessary condition for tackling climate change.

December 2022’s UN Biodiversity Conference in Montreal, also referred to as COP15, has raised the profile of biodiversity and its significance to achieving net zero, adding fresh impetus to our conversations with companies on this topic.

As our survey shows, businesses have not lost their stomach for the fight and have maintained their ESG emphasis during a tough 12 months. In 2023, we will continue to encourage managers to apply more of that energy to nature-related challenges like deforestation. There is much work to do but companies are listening – and acting.

Footnote:

1: Scope 1 2 3 Emissions Explained: Understanding the GHG Protocol’s Emission Classification System. Scope 1, 2, and 3 emissions are a way of categorising business emissions, accounting for both direct and indirect emitted greenhouse gasses (GHGs). Scope 1 emissions are GHGs released directly from a business. Scope 2 emissions are indirect GHGs released from the energy purchased by an organisation. Scope 3 emissions are also indirect GHG emissions, accounting for upstream and downstream emissions of a product or service, and emissions across a business’s value chain.