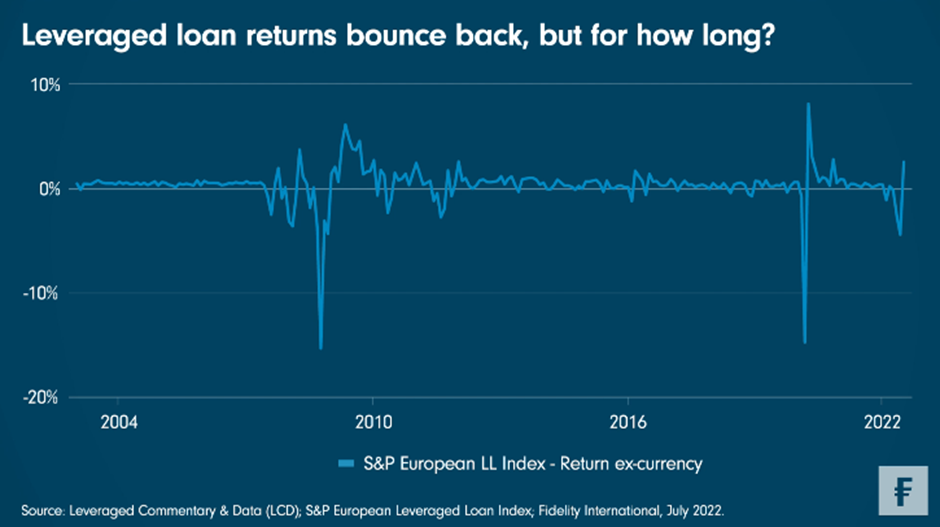

Returns in the European leveraged loan secondary market increased in July after a dramatic fall into negative figures running up to the end of June. But despite a step-up in demand over July pushing returns higher, conditions remain difficult and the current rise in the index could simply be a bear market rally.

The S&P European Leveraged Loan Index (ELLI) returned 2.56 per cent (excluding currency) in July after the market returned -4.43 per cent, one of the lowest monthly performances since the index’s inception, the month before. The July rally in loans reflected a wider market strengthening, with the last few weeks also seeing rising prices across equities and fixed income, but was also driven by a reopening of the market for new collateralised loan obligations (CLOs), with 8 deals being priced in July.

This week’s Chart Room shows that there have been two periods in the last 20 years when the secondary market has experienced large and sudden falls but then recovered quickly. In April 2020, as Covid-19 took hold, the index posted its second-lowest monthly return. The following month it recorded its highest ever return of 8.14 per cent. Similarly, the nadir of the Global Financial Crisis was followed by a run of positive monthly returns.

But past performance is not indicative of future results, and it may be that the index’s current swing upwards is more of a bear market rally than a sign of true recovery. Certainly, the market is likely to be hit by the poor corporate reporting expected in the third and fourth quarters, with recent profit warnings from both Walmart and Target giving early indications of the impact of waning consumer demand, while the negative drivers of the geopolitical concerns over the war in Ukraine, the continuing tightness of the US labour market, and high levels of inflation still hang over the market.

Primary transactions repricing

While there haven’t been enough syndicated deals recently to say definitively how far yields in the primary market have shifted as the secondary market index has moved up and down, the latest transactions suggest there has been a repricing of transactions in the primary sector.

Leveraged Commentary & Data (LCD) has reported that the most recent primary deals have not only come with higher margins, but also with a deep discount on the euro at issue, pushing initial yields higher. For example, a €365 million facility backing the buyout of distribution firm OptiGroup by FSN was priced in the primary market to yield 7.6 per cent with an original issue discount (OID) of 90, while a €500 million loan supporting Carlyle and PAI’s takeover of Theramex came with an OID of 94.75 to yield 6.36 per cent.

To put these pricing points into context, in the fourth quarter of 2021 the average yield on single-B rated European term loans was 4.59 per cent, according to LCD, with deals typically pricing at or close to par.

Direct lenders seek discounts

Yields on the latest deals in the primary market are not only far above what is typical for syndicated transactions. They are potentially higher than those usually commanded by direct lenders, who provide deals on a private basis without issuers having to brave the wider markets, typically commanding higher yields that reflects higher risk and leverage levels. With approximately €25 billion of deals now sitting on bank underwrite books according to LCD, it is no surprise that direct lenders are circling those transactions in the pipeline that are struggling to get syndicated, hoping to secure them at a discount.